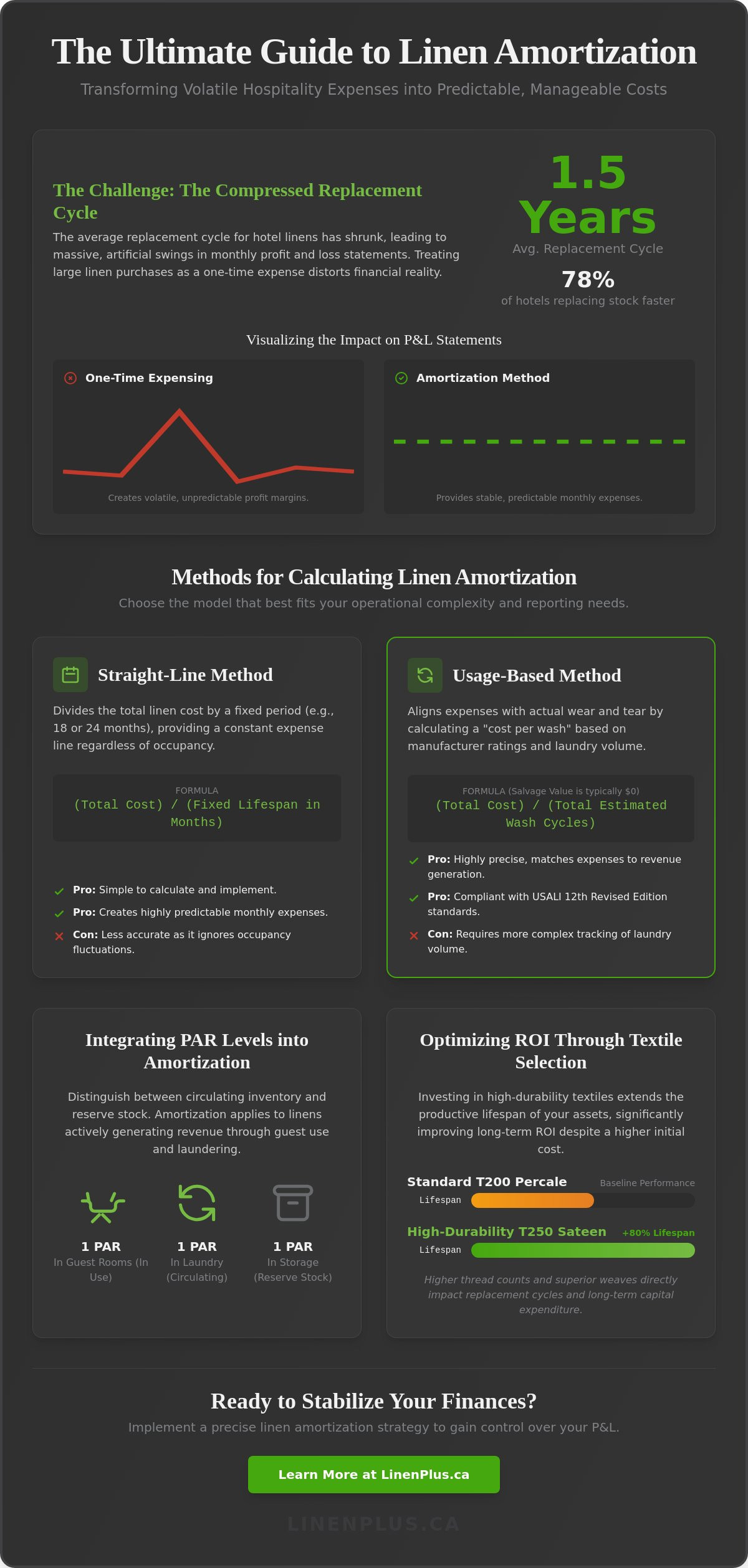

Did you know that the average replacement cycle for hotel linens in the U.S. has compressed to approximately 1.5 years? This shift means that 78% of mid-to-high-end properties are now replacing stock faster than ever, often creating massive, artificial swings in monthly profit and loss statements. If you're struggling with these volatile expenses, you aren't alone. Precise methods for calculating linen amortization for hospitality accounting are essential to turn these bulk capital outlays into predictable, manageable operating costs that reflect the actual wear and tear of your inventory.

You understand that fiscal accuracy is the backbone of a profitable facility, yet the gap between tax incentives and operational reality is widening. While the One Big Beautiful Bill Act (OBBBA) allows for 100% bonus depreciation on your tax returns as of 2025, your internal reporting must still reflect the actual useful life of your assets to remain compliant with the mandatory 12th Revised Edition of the USALI. This guide provides the technical framework you need to bridge that gap. We'll walk through specific calculation models that align your physical inventory loss with your financial statements, ensuring your cash flow forecasting remains as dependable as the service you provide to your guests.

Key Takeaways

- Understand why hospitality accounting treats linens as a unique asset class distinct from fixed furniture to prevent artificial swings in monthly P&L statements.

- Compare the technical advantages of Straight-Line versus Usage-Based methods for calculating linen amortization for hospitality accounting to better match expenses with guest turnover.

- Learn how to integrate PAR levels into your amortization schedule by distinguishing between circulating inventory and reserve stock in your asset register.

- Discover how specific textile specifications, such as thread count and weave, directly impact your replacement cycles and long-term capital expenditure forecasting.

- Identify the financial benefits of investing in high-durability options like T-250 Sateen bed sheets to extend the productive lifespan of your assets and improve total ROI.

Understanding the Role of Linen Amortization in Hospitality Finance

Linen amortization is the systematic allocation of textile costs over their productive lifespan. In hospitality accounting, linens occupy a unique space. They aren't permanent fixed assets like a lobby sofa, yet they aren't single-use disposables either. Because the average replacement cycle for hotel linens in the U.S. has shortened to approximately 1.5 years, treating them as a one-time expense creates volatile monthly profit and loss (P&L) statements. Understanding Depreciation principles helps managers realize that while linens are tangible assets, their high turnover requires a specific amortization schedule rather than a standard 7-year depreciation window.

Properly calculating linen amortization for hospitality accounting ensures that a massive bulk purchase doesn't artificially deflate your margins in a single month. Instead, the cost is spread across the periods where the linens actually generate guest revenue. This practice aligns with the 12th Revised Edition of the Uniform System of Accounts for the Lodging Industry (USALI), which becomes mandatory on January 1, 2026. By following these standards, properties maintain financial transparency and ensure their reporting is consistent with modern industry benchmarks. This structural approach prevents the "P&L swings" that often frustrate owners and stakeholders during heavy procurement quarters.

Expensing vs. Amortizing: When to Switch?

Deciding when to move from immediate expensing to a formal amortization schedule often depends on the scale of your operation. Small properties with consistent, low-volume purchases might continue expensing linens as they're placed in service. However, larger facilities typically choose between two primary paths:

- The Inventory Method: You record purchases as an asset and expense the difference between opening and closing physical counts. This is highly accurate but labor-intensive.

- The Monthly Amortization Method: You spread the total cost of a bulk purchase over a predetermined period, such as 18 or 24 months, based on historical wear data.

Most mid-to-high-end hotels prefer the monthly method. It provides the most predictable expense line. This predictability is critical for accurate cash flow forecasting and maintaining operational stability across the fiscal year.

Methods for Calculating Linen Amortization and Depreciation

Selecting the right mathematical model is critical for calculating linen amortization for hospitality accounting. Most properties lean toward the Straight-Line Method because of its simplicity. You divide the total cost of the linen purchase by a fixed period, usually 12, 24, or 36 months. This provides a steady expense line every month regardless of occupancy. While simple, it doesn't always reflect the physical reality of the asset's degradation.

Need Reliable Wholesale Supplies for Your Facility?

Hotels, healthcare facilities, restaurants, and commercial operations across Canada trust Linen Plus for consistent bulk supply and commercial-grade quality.

Bulk Wholesale Pricing

Competitive pricing for large-volume procurement.

Reliable Nationwide Supply

Consistent inventory and fast shipping across Canada.

Hospitality & Healthcare Grade

Products designed for demanding commercial environments.

Alternatively, the Usage-Based Method offers higher precision by aligning depreciation with actual wear. This approach is supported by academic Hotel Depreciation Studies, which highlight how usage frequency impacts the lifespan of soft goods. You also need to factor in "rag-out" rates. These rates account for inventory that is stained, damaged, or stolen before it reaches its expected end-of-life. For accounting purposes, the salvage value of hospitality linens is typically zero since worn-out sheets have no resale value.

Step-by-Step Usage-Based Calculation

To implement this, you first need to determine the average lifespan of your textiles. For example, high-quality T200 Percale Bed Sheets are often rated for a specific number of industrial wash cycles. The formula is: (Total Cost - Salvage Value) / Estimated Total Wash Cycles. This gives you a "cost per wash" that you apply to your monthly laundry volume.

- Identify the Rating: Use the manufacturer's wash-cycle rating for your specific sheet or towel.

- Track Volume: Monitor monthly occupancy to determine how many times each PAR was laundered.

- Adjust for Reality: Review the amortization rate quarterly to account for seasonal spikes or higher rag-out rates.

This method ensures your expenses rise and fall in direct proportion to your revenue. If you're looking to simplify your procurement while maintaining these standards, you can browse professional-grade bed linens designed for high-cycle durability to ensure your calculations remain accurate over time.

Integrating PAR Levels into Your Amortization Schedule

PAR levels represent the baseline inventory required to service a property without operational delays. A standard 3-PAR system includes one set in the guest room, one set in the laundry, and one set in storage. When calculating linen amortization for hospitality accounting, your chosen PAR level dictates the size of your initial capital investment. Moving to a 5-PAR system increases upfront costs but significantly extends the useful life of each item. This happens because individual linens are laundered less frequently, reducing the mechanical stress that leads to "rag-out" status.

Your asset register should distinguish between "circulating" and "reserve" inventory. Amortization should only begin when an item is placed into circulation. Reserve stock held in a central warehouse remains a current asset at its full purchase price until it's released to the floors. This distinction ensures your financial reporting accurately reflects the actual wear occurring in your facility. For those establishing new properties, selecting the right hospitality supply program helps stabilize these opening stock valuations from day one.

Valuing Your Opening Stock

Most hospitality managers use either the Weighted Average Cost or the First-In, First-Out (FIFO) method to value their linen inventory. FIFO is often preferred because it assumes the oldest stock is used first, which matches the physical rotation of linens in a well-managed laundry. To maintain the integrity of your books, you must conduct a physical linen count at least quarterly. This count reconciles the physical inventory on hand with the remaining value on your amortization schedule. If your physical count shows a significant deficit, you must adjust your amortization rate to account for higher-than-expected loss or damage.

Maintaining accurate counts across multiple PARs is the only way to ensure your balance sheet remains reliable. If you're ready to optimize your inventory, you can order bulk hospitality linens to replenish your PAR levels and maintain a consistent amortization cycle.

Optimizing ROI through Strategic Textile Selection

The physical specifications of your inventory are just as important as the mathematical formulas used in your ledger. Thread count and weave construction directly dictate the durability of the fabric, which in turn determines the length of your amortization period. For instance, percale weaves offer a crisp feel but have different tensile strength profiles compared to sateen. Investing in T-250 Sateen Bed Sheets often yields a lower long-term replacement cost because the tighter weave pattern can withstand more industrial wash cycles before thinning. This durability allows you to stretch the amortization schedule from 12 months to 18 or even 24 months, directly improving your bottom line.

Reducing your "Cost per Use" requires sourcing textiles engineered for the rigors of commercial laundering. High-tensile strength fibers and bleach-guard technologies protect the asset from chemical degradation, which is a leading cause of premature "rag-out" status. High-quality bath towels featuring double-stitched hems extend the amortization window by preventing edge fraying during high-heat drying cycles. When you select products based on these technical specifications, calculating linen amortization for hospitality accounting becomes more than just a compliance task; it's a tool for strategic growth.

Bulk Procurement and Fiscal Planning

Standardizing linen types doesn't just simplify inventory; it streamlines the entire procurement pipeline. When every room uses the same specifications, you can apply a uniform rate for calculating linen amortization for hospitality accounting, reducing the complexity of your asset register. This uniformity allows for better volume-based pricing and more predictable replacement schedules. Data-driven amortization provides the evidence needed to justify the budget for premium hospitality supplies. By demonstrating that a higher upfront investment in durable goods leads to a lower monthly depreciation expense, operations managers can make a compelling case for quality over initial price. This approach ensures your procurement strategy supports long-term fiscal health and operational excellence.

Mastering Your Textile Lifecycle for Long-Term Profitability

Transitioning from bulk expensing to precise amortization is a requirement for any facility aiming for financial maturity. By aligning your accounting with the physical reality of your inventory, you eliminate the unpredictable budget spikes that often follow a major linen refresh. Mastering the technical side of calculating linen amortization for hospitality accounting allows you to forecast capital expenditures with confidence while maintaining the high standards your guests expect. Success in this area relies on the intersection of accounting precision and product quality.

High-durability textiles, such as our industry-leading T200 and T250 standards, are specifically engineered to survive the industrial wash cycles that typically shorten an asset's lifespan. We support your operational goals through direct manufacturer partnerships that ensure a lower cost-per-cycle and reliable national Canadian distribution for consistent PAR replenishment. Optimize your linen ROI with our hospitality procurement solutions and secure the high-quality stock your facility requires. With the right data and the right supplies, you'll transform your linen closet from a cost center into a well-managed, predictable asset.

Frequently Asked Questions

Is linen considered a fixed asset or an operating expense in hotel accounting?

Under the Uniform System of Accounts for the Lodging Industry (USALI), linens are generally treated as an operating supply rather than a fixed asset. They are recorded as a current asset on the balance sheet and then amortized into the operating expense account over their useful life. This differs from fixed assets like furniture, which have a much longer depreciation schedule. Smaller properties may choose to expense them immediately if the purchase price is below their internal capitalization threshold.

How many wash cycles should a standard hotel sheet last before it is fully amortized?

A standard hospitality sheet typically lasts between 100 to 150 industrial wash cycles. The specific number depends on the fabric composition, such as whether you use T200 percale or T250 sateen. When calculating linen amortization for hospitality accounting using the usage-based method, managers track these cycles to retire the asset value once the textile reaches its physical threshold for guest-ready quality. This ensures your books reflect actual wear and tear rather than arbitrary dates.

What is the most common amortization period for hospitality linens in Canada?

Most Canadian properties use an amortization period between 12 and 24 months. This timeline aligns with the 1.5-year replacement cycle currently observed across the industry. While some properties stretch this to 36 months for reserve stock, the accelerating guest expectations for hygiene and comfort often make the 18-month mark the most realistic fiscal target for high-traffic facilities. Accurate local logistics also play a role in how quickly you can replenish these assets when they expire.

How do I account for linen loss and theft in my amortization calculation?

You account for loss and theft by including a shrinkage percentage in your monthly expense. This rate usually ranges between 5% and 10% of your total inventory value annually. When performing quarterly physical counts, you must adjust your amortization schedule to reflect these missing items. This reconciliation prevents your balance sheet from overstating the value of your circulating stock. It also helps you identify if theft rates are exceeding your operational benchmarks and require security adjustments.

Does thread count actually affect the financial depreciation of bed sheets?

Yes, thread count directly impacts the financial depreciation rate by determining the textile's physical longevity. Higher thread counts, like T250 sateen, generally feature more durable weaves that resist thinning and fraying longer than lower-count alternatives. By choosing more durable materials, you can justify a longer amortization period. This lowers your monthly expense and stabilizes your profit margins over the asset's lifespan. It turns a procurement decision into a strategic financial advantage for the property.

Article by

Sohel Shahriar

Sohel Shahriar is the Chief Growth Officer (CGO) at Linen Plus Inc., Canada, bringing a strategic blend of growth marketing, brand leadership, and content expertise. Through his writing, he explores how quality linen, smart sourcing, and long‑term partnerships can create measurable impact for healthcare and hospitality organizations.